Sector Coverage — Reclimatize.in

Steel

India is the world’s second largest steel producer, but most of that steel is made through the blast furnace route — one of the most carbon-intensive production processes in industry. That fact is now a trade and financial risk, not just an environmental one. The EU Carbon Border Adjustment Mechanism makes it a commercial problem from 2026.

India’s steel industry sits at the sharpest end of the industrial decarbonisation challenge. It is a Designated Consumer under the PAT Scheme, subject to Renewable Purchase and Consumption Obligations, required to obtain environmental clearance for new capacity, and from 2026 exposed to CBAM levies on every tonne of steel exported to the EU. The Ministry of Steel has publicly acknowledged that CBAM poses a larger risk to the sector than US tariffs — and that is before EU ETS carbon prices rise further.

The core problem is production route. Around 55% of India’s steel is produced via the blast furnace-basic oxygen furnace route, which burns metallurgical coal and generates roughly 2.5 tonnes of CO₂ per tonne of finished steel — well above where the sector needs to be. The Indian government introduced a Green Steel Taxonomy in December 2024, classifying steel with emissions below 2.2 tCO₂/t as green and below 1.6 tCO₂/t as five-star. The gap between current BF-BOF performance and those thresholds is large for most producers, which is why planning the transition now matters.

For a visual overview of all the regulations that apply to steel alongside other sectors, see the Industrial Decarbonisation Policy Map. For India’s broader climate commitments and NDC targets that frame the sector’s long-term direction, see the India Decarbonisation page. To explore all five covered sectors together, visit the Sectors overview.

Policy Pressures on the Sector

Steel producers navigate multiple simultaneous regulatory obligations. These are the ones that matter most right now.

EU Carbon Border Adjustment Mechanism

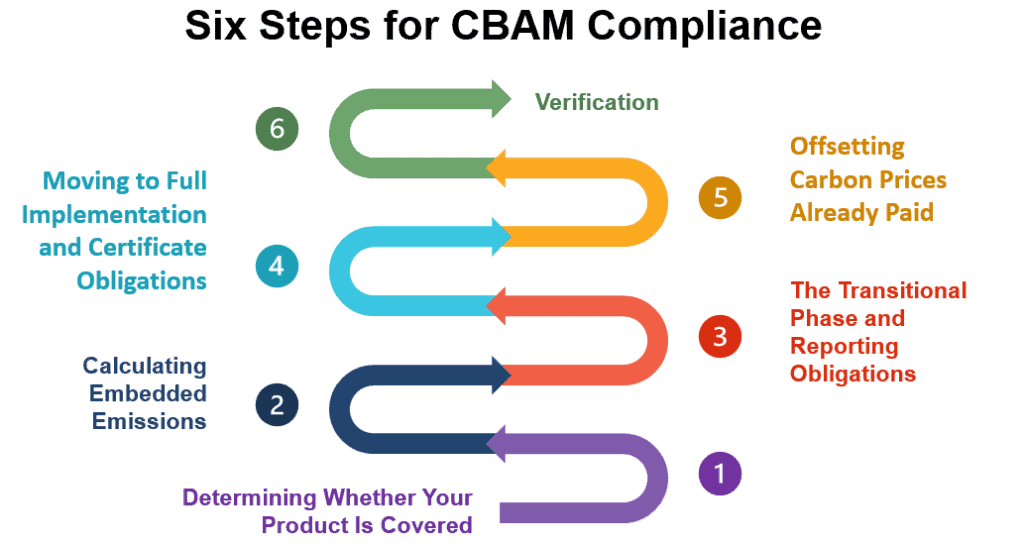

Steel and iron is India’s largest CBAM-covered export category to the EU. From January 2026, EU importers must purchase CBAM certificates for the embedded emissions in each tonne of Indian steel. Producers running blast furnaces will face material levies that competitors in countries with lower-carbon steel production will not. Studies suggest exporters may need to cut prices by 15 to 22% to absorb the cost if they do not reduce their carbon intensity — which is not a sustainable commercial position.

Read our CBAM analysisHow CBAM works operationally

PAT Scheme and Carbon Credit Trading Scheme

Steel plants above the designated threshold are Designated Consumers under the PAT Scheme, with mandatory Specific Energy Consumption targets set for each three-year cycle. Those who miss targets must buy Energy Saving Certificates. As the Carbon Credit Trading Scheme operationalises, steel sector compliance will expand from energy intensity targets to carbon credit obligations, increasing both the complexity and the financial stakes of performance gaps. The Bureau of Energy Efficiency administers both mechanisms.

Carbon Markets repositoryRenewable Purchase and Consumption Obligations

Steel producers must source a rising share of their electricity from renewable sources under the RPO framework and the Renewable Consumption Obligation introduced in the Energy Conservation (Amendment) Act 2022. For steel plants operating captive power plants — common in the integrated BF-BOF sector — the Green Energy Open Access Rules and the ISTS waiver are the primary tools for sourcing renewable power cost-effectively. State-level policies matter significantly here — see the State Renewable Policies page for how Odisha, Chhattisgarh and Jharkhand compare.

Renewable Obligations repositoryAir Act, EIA and Fly Ash Utilisation

Steel plants face stack emission standards for particulate matter, sulphur dioxide and nitrogen oxides under the Air (Prevention and Control of Pollution) Act, requiring ongoing investment in pollution control equipment. New capacity requires environmental clearance under the EIA Notification from the Ministry of Environment, Forest and Climate Change. Steel is also a major fly ash consumer — the Fly Ash Utilisation Notification links steel plants to nearby thermal power stations.

Environmental Regulations repositoryThe decarbonisation pathway for Indian steel

There is no single technology that decarbonises steel. The realistic pathway is a combination of near-term renewable electricity switching, medium-term scrap-based EAF expansion and long-term hydrogen-based direct reduced iron.

Near term

Renewable electricity and efficiency

Switching captive power from coal to renewable electricity reduces Scope 2 emissions and improves the Green Steel Taxonomy rating. Solar and wind tariffs below Rs 2.50/unit make this commercially attractive alongside being a compliance lever for RPO and RCO obligations.

Medium term

Scrap-based electric arc furnace expansion

EAF production using steel scrap emits roughly 0.4 to 0.6 tCO₂/t — well below both CBAM benchmarks and BF-BOF averages. India’s scrap availability is growing as the country’s steel stock ages, though EU scrap export restrictions may constrain supply for Indian EAF producers over time.

Long term

Hydrogen-based direct reduced iron

Replacing coking coal with green hydrogen in the DRI process eliminates process emissions from ironmaking. H2-DRI is technically proven but commercially dependent on green hydrogen becoming available at scale under the National Green Hydrogen Mission and SIGHT programme.

Key external references

Official government sources, research institutions and international bodies tracking India’s steel sector decarbonisation.

Ministry of Steel, India

Official policy notifications, Green Steel Taxonomy, sector statistics

BEE — PAT Scheme

Official PAT programme page, designated consumer lists, ESCert trading

IEA — Iron and Steel Technology Roadmap

Global decarbonisation pathways, technology costs, emission benchmarks

World Steel Association

Global production data, CO₂ intensity benchmarks, industry statistics

European Commission — CBAM

Official CBAM regulation text, product coverage, reporting obligations

IEEFA — India Steel Research

Independent analysis of steel sector financing and transition economics

Regulations that apply to this sector

Steel producers sit at the intersection of carbon, efficiency, electricity, environmental and trade regulations simultaneously. These repository pages cover each area in detail with official government links.

Other sectors we cover

Steel does not sit in isolation. Its decarbonisation economics connect directly to the power sector, carbon markets and freight logistics.

Latest Research on Steel

Analysis and commentary on steel sector decarbonisation, CBAM exposure and energy transition economics in India. Also see our full Research section.

How the Carbon Border Adjustment Mechanism Works: A Guide for Exporters