Sector Coverage — Reclimatize.in

Fertilisers

India’s fertiliser industry is built on natural gas. The gas goes in, ammonia comes out, and then urea. Decarbonising the sector means replacing that gas with green hydrogen — which is technically straightforward but economically still a significant stretch at current costs. The EU CBAM is now forcing the timeline.

The fertiliser sector’s decarbonisation problem is a feedstock problem. Ammonia synthesis — the first step in making urea and other nitrogenous fertilisers — requires hydrogen. Today that hydrogen comes from natural gas through the steam methane reforming process, generating substantial CO₂ as a by-product. Replacing this grey hydrogen with green hydrogen produced from renewable electricity-powered electrolysis is the only credible route to decarbonising the sector at scale. The National Green Hydrogen Mission and its SIGHT programme are the primary policy instruments targeting this transition.

There is also an energy security dimension that is often overlooked. Around 86% of India’s ammonia requirement was import-dependent in FY 2022-23, and over 60% of gas consumed in the sector comes from imported LNG. Global gas price spikes translate directly into higher fertiliser subsidies for the government — India spent over Rs 2.25 lakh crore on fertiliser subsidies in FY 2022-23 alone. Green hydrogen produced domestically from renewable electricity eliminates that import dependency and subsidy volatility, which is why the Ministry of New and Renewable Energy has made fertilisers the primary target for the Hydrogen Purchase Obligation.

See the Industrial Decarbonisation Policy Map for a full view of how all these regulations interact. For India’s NDC targets and climate commitments that shape the long-term policy direction, see the India Decarbonisation page. To compare the fertiliser sector with the other four sectors we cover, visit the Sectors overview.

Policy Pressures on the Sector

The fertiliser sector faces a distinct combination of trade, hydrogen, carbon and energy policy pressures that no other covered sector matches.

EU Carbon Border Adjustment Mechanism

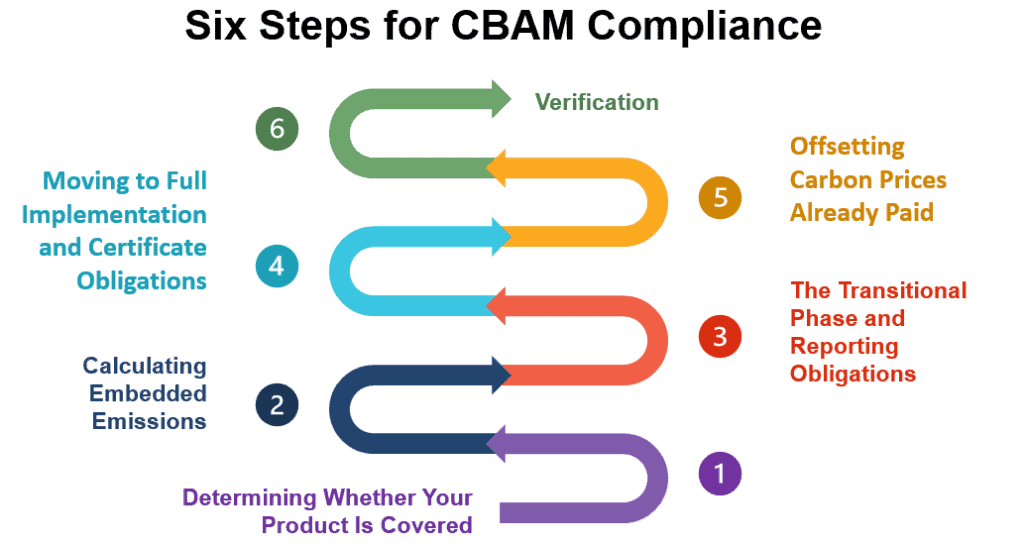

Nitrogenous fertilisers — urea, ammonia, nitric acid and ammonium nitrate — are among the six product categories covered by CBAM. From January 2026, EU importers must purchase certificates for the embedded emissions in each tonne. India’s urea and ammonia exports carry some of the highest embedded emission intensities of any CBAM-covered product, given the steam methane reforming process. Producers targeting the EU market face an immediate financial incentive to begin the green ammonia transition or risk losing export competitiveness to lower-carbon competitors in the Middle East and North Africa.

Read our CBAM analysisHow CBAM works operationally

National Green Hydrogen Mission and SIGHT

The fertiliser sector is the primary target for the Hydrogen Purchase Obligation — the proposed mechanism that will mandate minimum green hydrogen procurement. The SIGHT programme provides production incentives of Rs 8.82/kg for the first year declining over three years, designed to narrow the cost gap with grey hydrogen. SECI has issued tenders and awarded capacity specifically targeting fertiliser applications, with 10-year offtake agreements providing revenue certainty for early-mover producers. The second major SECI tender awarded 450,000 tonnes per year of green hydrogen capacity in March 2025.

Green Hydrogen repositoryPAT Scheme and Carbon Credit Trading Scheme

Fertiliser plants above the threshold are Designated Consumers under the PAT Scheme, administered by the Bureau of Energy Efficiency, with mandatory Specific Energy Consumption targets. Given that 70 to 80% of urea production cost is gas-related, energy efficiency improvements in the reforming and synthesis processes have significant commercial value beyond mere compliance. The emerging Carbon Credit Trading Scheme will add another compliance layer as it operationalises.

Carbon Markets repositoryAir Act and Hazardous Waste Rules

Ammonia plants are subject to stack emission standards for particulate matter, nitrogen oxides and ammonia fugitive emissions under the Air Act, requiring ongoing investment in pollution control equipment. The handling, storage and disposal of hazardous industrial waste — including spent catalysts from reforming units — is governed by the Hazardous Waste Management Rules administered by MoEFCC. New plant capacity requires EIA clearance.

Environmental Regulations repositoryThe decarbonisation pathway for Indian fertilisers

Unlike steel or aluminium, the fertiliser sector has a relatively clear single pathway: replace grey ammonia with green ammonia. The question is sequencing and economics, not technology choice.

Near term

Green ammonia blending in non-urea fertilisers

Complex fertilisers like ammonium sulphate and DAP do not need CO₂ as a feedstock the way urea does, making green ammonia blending technically simpler. This is the most viable early adoption pathway and is the focus of current SECI tenders. A 10% blend in non-urea fertilisers is economically feasible with current SIGHT incentives.

Medium term

Hybrid grey-green ammonia in urea plants

Urea production requires CO₂ as well as ammonia, and that CO₂ currently comes as a by-product of grey hydrogen reforming. A full switch to green ammonia in urea plants requires an external CO₂ source from nearby cement plants, steel mills or power stations. Blending 25% green ammonia in existing plants in hybrid mode is achievable within the next decade.

Long term

Greenfield green ammonia plants with CO₂ capture

Fully green urea plants require electrolysers, renewable electricity and an external CO₂ pipeline from industrial point sources. India has the renewable resource base and industrial cluster density to make this viable. Research has mapped CO₂-emitting plants within 150 km of most major urea facilities.

Key external references

Official government sources and research institutions tracking fertiliser sector decarbonisation in India.

MNRE — National Green Hydrogen Mission

Mission framework, SIGHT programme, HPO development

SECI — Green Hydrogen Tenders

Active and completed tenders for green hydrogen and ammonia production

Department of Fertilisers, India

Official fertiliser policy, subsidy framework and sector statistics

BEE — PAT Scheme

Designated consumer lists and SEC targets for fertiliser plants

European Commission — CBAM

Official CBAM regulation text and fertiliser product coverage

IEA — Ammonia Technology Roadmap

Global decarbonisation pathways and green ammonia cost trajectories

Regulations that apply to this sector

The fertiliser sector’s regulatory obligations span carbon markets, hydrogen policy, energy efficiency and environmental compliance simultaneously.

Other sectors we cover

The fertiliser sector’s decarbonisation is closely tied to the power sector through its renewable electricity needs and to steel through shared carbon market obligations.

Latest Research on Fertilisers

Analysis of the fertiliser sector’s CBAM exposure, green hydrogen transition economics and policy developments in India. Also see our full Research section.

How the Carbon Border Adjustment Mechanism Works: A Guide for Exporters