Sector Coverage — Reclimatize.in

Aluminium

Aluminium smelting runs almost entirely on electricity. That makes the sector’s carbon footprint almost entirely a function of where that electricity comes from. In India, most of it still comes from captive coal power plants — and that is the problem that CBAM and renewable obligations are now forcing the sector to confront.

The aluminium sector’s decarbonisation story is deceptively simple: approximately 80% of its emissions come from the electricity used to power the electrolysis process, and almost all of that electricity in India comes from captive coal-fired power plants. Switching from coal-based captive power to renewable electricity is the single most impactful lever available to the sector — and it is increasingly commercially attractive given solar and wind tariffs below Rs 2.50 per unit in competitive auctions facilitated by the National Solar Mission.

The CBAM complication is important to understand correctly. The EU’s rules currently cover only direct emissions from the electrolysis process itself, not the indirect emissions from electricity generation — which is where 80% of India’s aluminium emissions actually sit. This means Indian producers initially face CBAM levies only on their direct process emissions. But as the EU methodology potentially expands to indirect emissions and EU ETS prices rise, the pressure will increase. Early movers on renewable power procurement through open access are building a structural cost and competitiveness advantage now.

See the Industrial Decarbonisation Policy Map for a full view of how these regulations interact across the sector. For India’s broader NDC targets and climate commitments, see the India Decarbonisation page. To compare aluminium with the other four covered sectors, visit the Sectors overview.

Policy Pressures on the Sector

Aluminium producers face energy, carbon and environmental obligations alongside the CBAM trade pressure.

EU Carbon Border Adjustment Mechanism

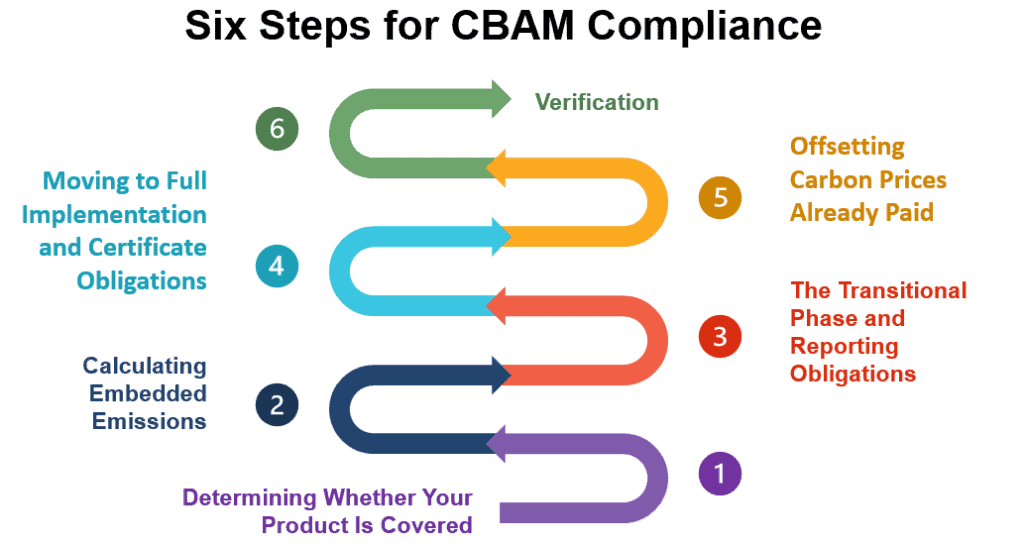

India exports approximately 0.7 MMTPA of aluminium to Europe. Under CBAM, EU importers must purchase certificates for the embedded direct emissions in each tonne. The CBAM benchmark emission intensity of 1.55 tCO₂/t for electrolysis means Indian smelters dependent on coal-based power will face increasing levies as EU ETS carbon prices rise. The key strategic variable is whether producers can shift to renewable power fast enough to improve their direct emission intensity before the levies become material.

Read our CBAM analysisHow CBAM works operationally

Open Access and Renewable Obligations

The Green Energy Open Access Rules 2022 and the ISTS waiver create the policy conditions for aluminium producers to procure renewable electricity cost-effectively, including from distant wind and solar generators in Rajasthan and Gujarat. The Renewable Consumption Obligation under the Energy Conservation (Amendment) Act 2022 requires designated industrial consumers to source a minimum and growing share of their energy from non-fossil sources. The CERC’s open access regulations govern how cross-state transactions are structured.

Electricity Market repositoryPAT Scheme and Energy Saving Certificates

Aluminium smelters are Designated Consumers under the PAT Scheme, with mandatory Specific Energy Consumption targets set by the Bureau of Energy Efficiency. The sector’s electricity intensity has improved significantly since 2010, but most primary smelters are already close to best available technology in electrolysis efficiency, meaning future PAT performance gains depend more on power supply decarbonisation than process improvements. The emerging Carbon Credit Trading Scheme will add another compliance and market interaction layer.

Carbon Markets repositoryAir Act and EIA Notification

Aluminium smelters and associated refineries are subject to stack emission standards under the Air (Prevention and Control of Pollution) Act and effluent discharge limits under the Water Act, administered by State Pollution Control Boards under the Ministry of Environment, Forest and Climate Change. New smelter capacity and refinery expansions require environmental clearance under the EIA Notification. For producers in Odisha and Chhattisgarh, state-level environmental regulations add an additional layer of compliance planning.

Environmental Regulations repositoryThe decarbonisation pathway for Indian aluminium

Unlike steel, aluminium’s decarbonisation is fundamentally an electricity problem — which means it is solvable through renewable procurement. The pathway is relatively clear even if execution is not easy.

Near term

Round-the-clock renewable power procurement

Wind-solar hybrid projects with storage deliver power across more hours of the day than either source alone. Long-term PPAs for hybrid projects, combined with the ISTS waiver for cross-state procurement, are the most immediately viable path to reducing coal CPP dependence under the Wind-Solar Hybrid Policy.

Medium term

Captive renewable generation and storage

Large smelter complexes in coastal states like Odisha have access to land and grid infrastructure that makes on-site or nearby solar and wind development viable. Battery storage integrated with captive renewable generation can reduce coal CPP dependence without compromising operational continuity. The Energy Storage Obligation is creating the supply chain for this.

Long term

Nuclear and CCUS for residual emissions

NITI Aayog’s aluminium decarbonisation roadmap identifies nuclear power in the medium term and carbon capture utilisation and storage for residual coal-based captive plant emissions as long-term pathways for emissions that renewable electricity alone cannot eliminate.

Key external references

Official government sources and research institutions tracking aluminium sector decarbonisation in India and globally.

BEE — PAT Scheme

Designated consumer lists, SEC targets and ESCert trading for aluminium

Ministry of New and Renewable Energy

RPO trajectory, open access notifications and renewable energy programmes

IEA — Aluminium

Global decarbonisation pathways, electricity intensity benchmarks

World Aluminium

Global production data, CO₂ intensity benchmarks, industry statistics

European Commission — CBAM

Official CBAM regulation text, aluminium product coverage and benchmarks

CERC — Open Access Regulations

Inter-state open access rules and REC mechanism for industrial consumers

Regulations that apply to this sector

Aluminium producers face obligations across electricity, carbon, efficiency and environmental regulation simultaneously. These repository pages cover each area with official links.

Other sectors we cover

Aluminium’s decarbonisation connects directly to power market dynamics, carbon pricing and India’s green hydrogen ambition.

Latest Research on Aluminium

Analysis of aluminium sector decarbonisation, open access economics, CBAM exposure and renewable procurement strategy in India. Also see our full Research section.

How the Carbon Border Adjustment Mechanism Works: A Guide for Exporters