How the Carbon Border Adjustment Mechanism Works: A Guide for Exporters

Introduction

There is a lot of discussion about what the Carbon Border Adjustment Mechanism means for global trade.

Far less attention, however, has been paid to a more practical question: how does it actually work?

For exporters, particularly those in energy intensive industries, understanding the operational mechanics of CBAM is not an academic exercise. It determines what data you need to collect, what you need to report, and eventually what you may need to pay.

This article walks through how CBAM works in practice, from product identification through to certificate obligations, without the policy jargon that makes most CBAM coverage difficult to act on.

For context on why CBAM was introduced and what it means for Indian industry at a strategic level, see our detailed overview: Carbon Border Adjustment Mechanism and Its Impact on Indian Industry.

Executive Summary

- CBAM requires importers of certain goods into the EU to account for the carbon emissions embedded in those products.

- The mechanism works in phases: a transitional reporting period first, followed by full financial adjustments tied to EU carbon prices.

- Covered sectors currently include steel, aluminium, cement, fertilisers, electricity and hydrogen.

- Embedded emissions must be calculated at the production level and verified by accredited bodies.

- Where a carbon price has already been paid in the country of origin, this can be offset against CBAM obligations.

- Companies that do not prepare early risk compliance gaps when financial adjustments begin.

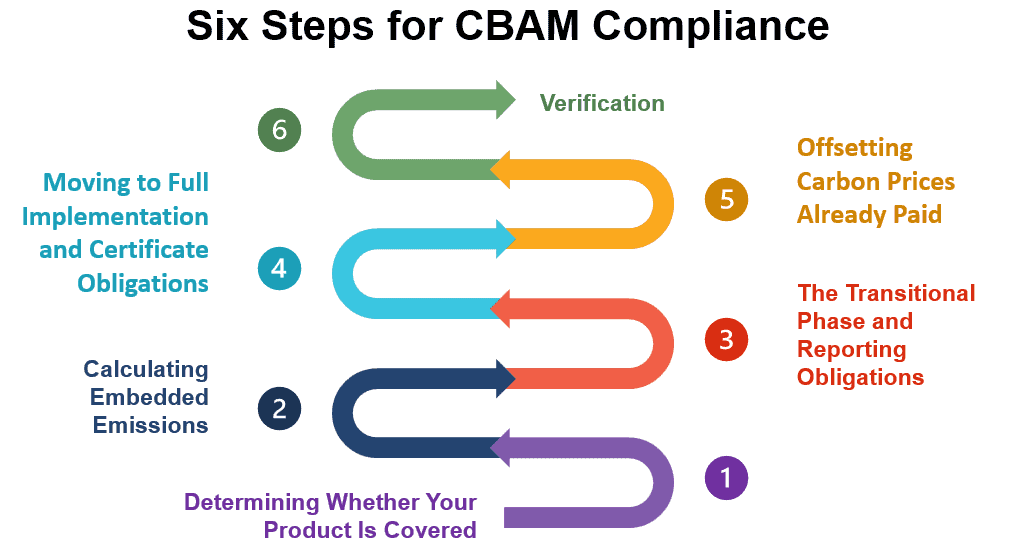

Step #1: Determining Whether Your Product Is Covered

CBAM does not apply to all goods. It currently covers a defined list of products within six sectors considered most vulnerable to carbon leakage.

Those sectors are steel and iron, aluminium, cement, fertilisers, electricity and hydrogen.

Coverage is defined by specific Combined Nomenclature (CN) codes, which are the EU’s product classification system. Exporters need to verify whether their specific products fall within the defined codes, because not every product within a broadly covered sector is automatically subject to CBAM.

This is a practical first step that many companies overlook. Assuming coverage without checking the actual CN classification can lead to either unnecessary compliance work or, worse, missing an obligation that does apply.

Step #2: Calculating Embedded Emissions

Once it is established that a product is covered, the next task is calculating its embedded emissions (refer to box below).

This distinction matters enormously for sectors like aluminium, where electricity accounts for a very large share of the production cost and emissions footprint. A smelter powered by coal based electricity will have a very different embedded emissions figure than one sourcing power from renewables, even if the physical production process is identical.

The EU has published default values that importers can use if actual production data is not available. However, using default values typically results in a higher assumed emissions figure, which translates into higher compliance costs.

Companies with genuinely lower than average emissions have a financial incentive to invest in proper measurement systems and document their actual production data.

Step #3: The Transitional Phase and Reporting Obligations

CBAM is not being switched on overnight. The EU has structured a transitional phase to allow companies time to build the necessary reporting infrastructure.

During the transitional period, importers are not yet required to purchase CBAM certificates or make financial payments. The obligation at this stage is to report.

Specifically, importers must submit quarterly reports to EU authorities. These reports must include the total quantity of covered goods imported, the total embedded emissions associated with those goods, and any carbon price already paid in the country of origin.

This reporting phase serves two purposes.

- It builds the data infrastructure that the EU needs to operate the full mechanism.

- It gives exporters and importers time to establish measurement systems before financial obligations kick in.

The transitional phase is not a free pass. Companies that treat it as a bureaucratic formality and do nothing are building a compliance gap that will become costly once the mechanism moves to its next phase.

Step #4: Moving to Full Implementation and Certificate Obligations

When CBAM moves beyond the transitional phase, the financial mechanism activates.

Importers will be required to purchase CBAM certificates. Each certificate corresponds to one tonne of carbon dioxide equivalent embedded in an imported product.

The price of these certificates is directly linked to the weekly average auction price of allowances under the EU Emissions Trading System (ETS). This is intentional. The goal is to ensure that importers pay a carbon cost comparable to what EU producers pay under the ETS, so that no competitive advantage is created through lower regulatory standards in the country of origin.

The importer surrenders certificates annually, matching the total embedded emissions of the goods they imported during the previous year.

Step #5: Offsetting Carbon Prices Already Paid

One important provision within CBAM is the ability to offset carbon costs already paid in the exporting country.

If an exporter has already paid a carbon price in their home country, this can be deducted from the CBAM certificate obligation in the EU. The intent is to avoid double taxation on carbon.

For India, this has a direct implication. India is developing its carbon market framework, including the Carbon Credit Trading Scheme. As that domestic carbon pricing system matures, Indian exporters may be able to use domestic carbon costs to offset part of their CBAM obligations in Europe.

The exact mechanism for how foreign carbon prices are recognised and verified under CBAM is still being developed, but the principle of offset is already embedded in the regulation.

Step #6: Verification

CBAM is not a self declared system. Embedded emissions data submitted by importers must be verified by accredited third party bodies.

This verification requirement is significant for exporters. It means that internal emissions estimates alone will not be sufficient. Companies will need auditable data systems and the ability to work with independent verifiers to confirm that reported emissions figures are accurate.

For many mid-sized industrial exporters, this is the part of CBAM compliance that requires the most preparation time, because building credible emissions measurement systems is not something that can be done quickly.

Figure 1. Six Steps for CBAM Compliance

Source: Reclimatize Research, Design by PresentationGO.com

What This Means for Indian Exporters Practically

Taking all of these steps together, an Indian steel or aluminium exporter selling to Europe needs to do several things to prepare for CBAM.

They need to confirm which of their products fall under the defined CN codes and establish a system for measuring direct and, where applicable, indirect embedded emissions at the production level. They need to begin submitting quarterly reports during the transitional phase and work with accredited verifiers to confirm the accuracy of their emissions data. And they need to track domestic carbon pricing developments in India, because those will eventually be relevant to any offset calculation.

None of this is insurmountable. But none of it is simple either, particularly for companies that have not previously had to measure and report production-level emissions in any structured way.

Conclusion

CBAM is sometimes discussed as though it is primarily a political or trade policy question. Operationally, it is a data and compliance challenge.

The companies that will navigate it most effectively are the ones that treat the transitional reporting phase as genuine preparation time rather than a delay before the real obligations arrive. Building emissions measurement systems, understanding product-level coverage, and engaging with verification processes early will matter.

For Indian exporters in steel, aluminium and fertilisers, the window to prepare is open. The question is whether it gets used.

Frequently Asked Questions

How does the Carbon Border Adjustment Mechanism work?

CBAM requires importers bringing certain goods into the EU to report and eventually pay for the carbon emissions embedded in those products. The mechanism works in two phases: a transitional period focused on emissions reporting, followed by full implementation where importers must purchase CBAM certificates linked to EU carbon prices.

What are embedded emissions under CBAM?

Embedded emissions are the greenhouse gases produced during the manufacturing process of a product. Depending on the product, this may include direct emissions from production processes and indirect emissions from electricity used in manufacturing.

What are CBAM certificates?

CBAM certificates represent one tonne of carbon dioxide equivalent embedded in imported goods. Once the mechanism is fully operational, importers must purchase and surrender certificates each year to cover the embedded emissions of their imports.

Can a carbon price paid in the exporting country reduce CBAM obligations?

Yes. If an exporter has already paid a carbon price in their home country, this can be offset against the CBAM certificate obligation in the EU, to avoid double taxation on carbon emissions.

Which products are covered under CBAM?

CBAM currently covers specific products within the sectors of steel and iron, aluminium, cement, fertilisers, electricity and hydrogen. Coverage is defined by specific EU product classification codes.